---

title: "Chapter 3: Simple Linear Regression"

subtitle: "OLS estimation, matrix form, geometry, and goodness of fit"

---

```{r}

#| label: setup

#| include: false

library(tidyverse)

library(broom)

library(modelsummary)

library(patchwork)

library(wooldridge)

theme_set(theme_minimal(base_size = 13))

options(digits = 4, scipen = 999)

```

::: {.callout-note}

## Learning Objectives

By the end of this chapter you will be able to:

- State the simple linear regression model and interpret its components

- Derive the OLS estimator algebraically from first-order conditions

- Write the regression model and the OLS estimator in matrix form

- Explain OLS geometrically as an orthogonal projection onto the column space of $\mathbf{X}$

- Derive the normal equations $\mathbf{X'X}\hat{\boldsymbol{\beta}} = \mathbf{X'y}$ from the orthogonality principle

- Verify the algebraic properties of OLS residuals

- Derive the SST = SSE + SSR decomposition as a consequence of orthogonality

- Compute and interpret $R^2$ and the standard error of the regression

- Fit and interpret a regression model in R

:::

---

## The Population Regression Function

We want to understand how a variable $y$ (the **dependent variable**) relates to $x$ (the **independent variable** or **regressor**). The population model is:

$$

y_i = \beta_0 + \beta_1 x_i + u_i, \quad i = 1, 2, \ldots, n

$$

- $\beta_0$: the **intercept** — expected value of $y$ when $x = 0$

- $\beta_1$: the **slope** — the change in $y$ per unit increase in $x$, ceteris paribus

- $u_i$: the **error term** — all factors that determine $y$ other than $x$

The interpretation $\Delta y / \Delta x = \beta_1$ is valid only when $\Delta u / \Delta x = 0$: that is, when $x$ changes do not move the unobservables. This is the **ceteris paribus** requirement.

### The Population Regression Function

The **zero conditional mean assumption** $E[u \mid x] = 0$ implies:

$$

E[y \mid x] = \beta_0 + \beta_1 x

$$

This is the **population regression function (PRF)**. It describes the true conditional mean in the population. We never observe it; we estimate it from data. Estimating the PRF requires a random sample $\{(x_i, y_i) : i = 1, \ldots, n\}$.

### SLR Assumptions

| | Assumption | Statement |

|--|-----------|-----------|

| **SLR.1** | Linearity | $y = \beta_0 + \beta_1 x + u$ |

| **SLR.2** | Random sampling | $(x_i, y_i)$ are i.i.d. draws from the population |

| **SLR.3** | Sample variation in $x$ | $\sum(x_i - \bar{x})^2 > 0$ |

| **SLR.4** | Zero conditional mean | $E[u \mid x] = 0$ |

SLR.4 is the load-bearing assumption. Its violation produces **endogeneity** and makes $\hat{\beta}_1$ biased.

### What Is a Model?

Studying two random variables means modelling their joint distribution — which is data-intensive. The strategy here is more targeted: model the **conditional distribution** of $y$ given $x$, and in particular its conditional mean $E[y \mid x]$.

An **incomplete model** specifies only $E[y \mid x] = \beta_0 + \beta_1 x$. A **complete model** (the **Classical Linear Model**) further specifies:

$$

\text{Var}(u \mid x) = \sigma^2 \quad \text{(homoskedasticity)}

$$

$$

u \mid x \sim \mathcal{N}(0, \sigma^2) \quad \text{(normality)}

$$

this chapter we work with the incomplete model. The CLM assumptions are taken up in Chapters 4 and 5.

---

## OLS Estimation: Scalar Derivation

Given data $(x_1, y_1), \ldots, (x_n, y_n)$, we need to choose $\hat{\beta}_0$ and $\hat{\beta}_1$. OLS chooses the values that minimise the **sum of squared residuals**:

$$

\min_{b_0,\, b_1} \; S(b_0, b_1) = \sum_{i=1}^{n} (y_i - b_0 - b_1 x_i)^2

$$

**First-order conditions:**

$$

\frac{\partial S}{\partial b_0}\bigg|_{\hat{\beta}} = -2\sum_{i=1}^{n}(y_i - \hat{\beta}_0 - \hat{\beta}_1 x_i) = 0

$$

$$

\frac{\partial S}{\partial b_1}\bigg|_{\hat{\beta}} = -2\sum_{i=1}^{n} x_i(y_i - \hat{\beta}_0 - \hat{\beta}_1 x_i) = 0

$$

These two equations — the **normal equations** in scalar form — are:

$$

\sum_{i=1}^{n} \hat{u}_i = 0 \tag{1}

$$

$$

\sum_{i=1}^{n} x_i \hat{u}_i = 0 \tag{2}

$$

**Solving the system.** Dividing (1) by $n$ gives $\hat{\beta}_0 = \bar{y} - \hat{\beta}_1 \bar{x}$. Substituting into (2) and simplifying (see Wooldridge p. 28):

$$

\boxed{\hat{\beta}_1 = \frac{\sum_{i=1}^n (x_i - \bar{x})(y_i - \bar{y})}{\sum_{i=1}^n (x_i - \bar{x})^2} = \frac{\widehat{\text{Cov}}(x, y)}{\widehat{\text{Var}}(x)}}

$$

$$

\boxed{\hat{\beta}_0 = \bar{y} - \hat{\beta}_1 \bar{x}}

$$

Notice that $\hat{\beta}_1 = \hat{\sigma}_{xy} / \hat{\sigma}_x^2$: the OLS slope is the sample covariance of $x$ and $y$ divided by the sample variance of $x$. In finance, this same formula gives the market **beta** of a stock.

The **estimated regression line** is $\hat{y} = \hat{\beta}_0 + \hat{\beta}_1 x$. Since $\hat{\beta}_0 = \bar{y} - \hat{\beta}_1 \bar{x}$, the line always passes through the sample mean $(\bar{x}, \bar{y})$.

### Estimators We Have Seen

Every population moment has a sample analogue. The table below collects them:

| Population parameter | Estimator |

|---|---|

| $\mu_y = E[y]$ | $\bar{y} = \frac{1}{n}\sum y_i$ |

| $\sigma_y^2 = E[(y - \mu_y)^2]$ | $\hat{s}_y^2 = \frac{1}{n-1}\sum(y_i - \bar{y})^2$ |

| $\sigma_{xy} = E[(x-\mu_x)(y-\mu_y)]$ | $\hat{s}_{xy} = \frac{1}{n-1}\sum(x_i - \bar{x})(y_i - \bar{y})$ |

| $\rho_{xy} = \sigma_{xy}/(\sigma_x \sigma_y)$ | $\hat{r}_{xy} = \hat{s}_{xy}/(\hat{s}_x \hat{s}_y)$ |

| $\beta_1$ in $E[y\mid x] = \beta_0 + \beta_1 x$ | $\hat{\beta}_1 = \hat{s}_{xy}/\hat{s}_x^2$ |

| $\beta_0$ | $\hat{\beta}_0 = \bar{y} - \hat{\beta}_1\bar{x}$ |

In every case the estimator is a function of sample data only. Because the data are random, $\hat{\beta}_0$ and $\hat{\beta}_1$ are **random variables**: different samples from the same population will yield different estimates.

---

## Matrix Form of the Regression Model

For $n$ observations the model $y_i = \beta_0 + \beta_1 x_i + u_i$ for $i = 1, \ldots, n$ can be stacked:

$$

\underbrace{\begin{bmatrix} y_1 \\ y_2 \\ \vdots \\ y_n \end{bmatrix}}_{\mathbf{y} \; (n \times 1)}

=

\underbrace{\begin{bmatrix} 1 & x_1 \\ 1 & x_2 \\ \vdots & \vdots \\ 1 & x_n \end{bmatrix}}_{\mathbf{X} \; (n \times 2)}

\underbrace{\begin{bmatrix} \beta_0 \\ \beta_1 \end{bmatrix}}_{\boldsymbol{\beta} \; (2 \times 1)}

+

\underbrace{\begin{bmatrix} u_1 \\ u_2 \\ \vdots \\ u_n \end{bmatrix}}_{\mathbf{u} \; (n \times 1)}

$$

Compactly: $\mathbf{y} = \mathbf{X}\boldsymbol{\beta} + \mathbf{u}$.

The first column of $\mathbf{X}$ is a column of ones, which "carries" the intercept $\beta_0$. The matrix $\mathbf{X}$ and vector $\mathbf{y}$ are **observable**; $\boldsymbol{\beta}$ and $\mathbf{u}$ are **unobservable**.

### Extension to Multiple Regression

With $k$ regressors plus an intercept the model is identical in form:

$$

\mathbf{y} = \mathbf{X}\boldsymbol{\beta} + \mathbf{u}, \quad \mathbf{X} \in \mathbb{R}^{n \times (k+1)}, \quad \boldsymbol{\beta} \in \mathbb{R}^{k+1}

$$

The power of abstraction: four apparently distinct problems — returns to education, stock betas, house price prediction, electricity load forecasting — are all instances of the single problem "estimate $\boldsymbol{\beta}$ in $\mathbf{y} = \mathbf{X}\boldsymbol{\beta} + \mathbf{u}$ from a sample of observations."

---

## Geometry of OLS

This section gives the geometric interpretation of least squares. It is not in Wooldridge but is essential for understanding what OLS computes, why $\mathbf{X'\hat{u}} = \mathbf{0}$, and where the $SST = SSE + SSR$ decomposition comes from.

### Vectors and Inner Products

Think of $\mathbf{y} = (y_1, \ldots, y_n)' \in \mathbb{R}^n$ as a point (or arrow from the origin) in $n$-dimensional space.

**Length** of a vector $\mathbf{v} \in \mathbb{R}^n$:

$$

\|\mathbf{v}\| = \sqrt{\mathbf{v}'\mathbf{v}} = \sqrt{\sum_{i=1}^n v_i^2}

$$

**Orthogonality.** Two vectors $\mathbf{u}, \mathbf{v} \in \mathbb{R}^n$ are **orthogonal** (perpendicular) if and only if:

$$

\mathbf{u}'\mathbf{v} = \sum_{i=1}^n u_i v_i = 0

$$

### The Column Space of $\mathbf{X}$

For any $(k+1)$-vector $\mathbf{b}$, the product $\mathbf{Xb}$ is an $n$-vector that is a **linear combination of the columns of $\mathbf{X}$**. The set of all such vectors:

$$

\mathcal{C}(\mathbf{X}) = \{\mathbf{Xb} : \mathbf{b} \in \mathbb{R}^{k+1}\}

$$

is the **column space** (or **range**) of $\mathbf{X}$. It is a subspace of $\mathbb{R}^n$.

- If $\mathbf{X}$ has $k+1$ **linearly independent** columns, then $\mathcal{C}(\mathbf{X})$ is a $(k+1)$-dimensional flat (hyperplane through the origin) inside $\mathbb{R}^n$.

- With $k+1 < n$ (more observations than parameters — the usual case), this flat is a proper subspace: **$\mathbf{y}$ will generically not lie in $\mathcal{C}(\mathbf{X})$.**

### A Concrete Illustration

**Two observations, two parameters.** Suppose $n = 2$ and $\mathbf{X}$ has two linearly independent columns. Then $\mathcal{C}(\mathbf{X}) = \mathbb{R}^2$: every 2-vector $\mathbf{y}$ lies in $\mathcal{C}(\mathbf{X})$, so we can fit the data perfectly with zero residuals.

**Three observations, two parameters.** Now $n = 3$, $k+1 = 2$. $\mathcal{C}(\mathbf{X})$ is a 2-dimensional plane through the origin in $\mathbb{R}^3$. A generic $\mathbf{y} \in \mathbb{R}^3$ does **not** lie in this plane, so perfect fit is impossible.

```{r}

#| label: house-example

# Three houses: bedrooms = 4, 1, 1; prices = 10, 4, 6 (hundreds of thousands)

y <- c(10, 4, 6)

X <- cbind(1, c(4, 1, 1)) # [intercept | bedrooms]

# OLS: beta_hat = (X'X)^{-1} X'y

beta_hat <- solve(t(X) %*% X) %*% (t(X) %*% y)

y_hat <- X %*% beta_hat

u_hat <- y - y_hat

cat("beta_hat:", round(beta_hat, 4), "\n")

cat("y_hat: ", round(y_hat, 4), "\n")

cat("u_hat: ", round(u_hat, 4), "\n")

```

The residuals are non-zero: the data vector $\mathbf{y}$ does not lie in $\mathcal{C}(\mathbf{X})$.

### OLS as Orthogonal Projection

The OLS objective is:

$$

\min_{\mathbf{b}} \|\mathbf{y} - \mathbf{Xb}\|^2 = \min_{\mathbf{b}} \sum_{i=1}^n (y_i - \mathbf{x}_i'\mathbf{b})^2

$$

This is the problem of finding the point in $\mathcal{C}(\mathbf{X})$ **closest to $\mathbf{y}$** in Euclidean distance. The solution is the **orthogonal projection** of $\mathbf{y}$ onto $\mathcal{C}(\mathbf{X})$.

The projection $\hat{\mathbf{y}} = \mathbf{X}\hat{\boldsymbol{\beta}}$ is the unique point in $\mathcal{C}(\mathbf{X})$ such that the residual $\hat{\mathbf{u}} = \mathbf{y} - \hat{\mathbf{y}}$ is **perpendicular to the entire column space**:

$$

\hat{\mathbf{u}} \perp \mathcal{C}(\mathbf{X})

$$

::: {.callout-note}

## The Orthogonality Principle

$$\mathbf{X'}\hat{\mathbf{u}} = \mathbf{0}$$

The OLS residual vector is orthogonal to every column of $\mathbf{X}$. This single equation contains the entire geometry of OLS and is more important than any formula.

:::

The orthogonality condition says: the residual is uncorrelated with every regressor (including the constant). Writing it out column by column for $\mathbf{X} = [\mathbf{1}, \mathbf{x}_1, \ldots, \mathbf{x}_k]$:

$$

\mathbf{1}'\hat{\mathbf{u}} = \sum_{i=1}^n \hat{u}_i = 0

\qquad

\mathbf{x}_j'\hat{\mathbf{u}} = \sum_{i=1}^n x_{ij}\hat{u}_i = 0, \quad j = 1, \ldots, k

$$

These are exactly the scalar normal equations (1) and (2) we derived from the first-order conditions.

```{r}

#| label: orthogonality-check

# Verify X'u_hat = 0 for the house example

round(t(X) %*% u_hat, 10) # should be (0, 0)

```

### Deriving the OLS Formula

Substituting $\hat{\mathbf{u}} = \mathbf{y} - \mathbf{X}\hat{\boldsymbol{\beta}}$ into $\mathbf{X'}\hat{\mathbf{u}} = \mathbf{0}$:

$$

\mathbf{X}'(\mathbf{y} - \mathbf{X}\hat{\boldsymbol{\beta}}) = \mathbf{0}

$$

$$

\mathbf{X'y} = \mathbf{X'X}\hat{\boldsymbol{\beta}} \tag{Normal Equations}

$$

$$

\boxed{\hat{\boldsymbol{\beta}} = (\mathbf{X'X})^{-1}\mathbf{X'y}}

$$

provided $\mathbf{X'X}$ is invertible — which requires the columns of $\mathbf{X}$ to be **linearly independent** (no perfect multicollinearity).

### The Projection and Annihilator Matrices

Substituting back, the fitted values are:

$$

\hat{\mathbf{y}} = \mathbf{X}\hat{\boldsymbol{\beta}} = \mathbf{X}(\mathbf{X'X})^{-1}\mathbf{X'y} \equiv \mathbf{P}_X \mathbf{y}

$$

where $\mathbf{P}_X = \mathbf{X}(\mathbf{X'X})^{-1}\mathbf{X'}$ is the **hat matrix** (it puts the "hat" on $\mathbf{y}$). The residual vector is:

$$

\hat{\mathbf{u}} = \mathbf{y} - \hat{\mathbf{y}} = (\mathbf{I} - \mathbf{P}_X)\mathbf{y} \equiv \mathbf{M}_X \mathbf{y}

$$

where $\mathbf{M}_X = \mathbf{I} - \mathbf{P}_X$ is the **annihilator matrix**. Both $\mathbf{P}_X$ and $\mathbf{M}_X$ are symmetric and idempotent ($\mathbf{P}_X^2 = \mathbf{P}_X$, $\mathbf{M}_X^2 = \mathbf{M}_X$), and they are orthogonal to each other: $\mathbf{P}_X \mathbf{M}_X = \mathbf{0}$.

```{r}

#| label: projection-matrices

n <- nrow(X)

P <- X %*% solve(t(X) %*% X) %*% t(X) # hat matrix

M <- diag(n) - P # annihilator

# Idempotency: P^2 = P

cat("Max deviation P^2 - P:", max(abs(P %*% P - P)), "\n")

# Orthogonality: P M = 0

cat("Max deviation PM: ", max(abs(P %*% M)), "\n")

# y_hat and u_hat via projection

round(P %*% y, 4) # same as y_hat above

round(M %*% y, 4) # same as u_hat above

```

---

## Algebraic Properties of OLS

The orthogonality conditions $\mathbf{X'}\hat{\mathbf{u}} = \mathbf{0}$ have direct algebraic consequences. Writing out the two columns of $\mathbf{X} = [\mathbf{1}, \mathbf{x}]$:

**Property 1.** $\displaystyle\sum_{i=1}^n \hat{u}_i = 0$

The residuals sum to zero. OLS over-predicts as often as it under-predicts. (Follows from the column of ones being in $\mathbf{X}$.)

**Property 2.** $\displaystyle\sum_{i=1}^n x_i \hat{u}_i = 0$

The residuals are uncorrelated with the regressor in the sample.

**Property 3.** $\bar{y} = \hat{\bar{y}} = \hat{\beta}_0 + \hat{\beta}_1 \bar{x}$

The sample mean of fitted values equals the sample mean of $y$. The estimated regression line passes through $(\bar{x}, \bar{y})$.

```{r}

#| label: ols-properties

data("wage1", package = "wooldridge")

fit <- lm(wage ~ educ, data = wage1)

u <- residuals(fit)

x <- wage1$educ

cat("Sum of residuals: ", round(sum(u), 10), "\n")

cat("Cov(x, u_hat): ", round(sum(x * u), 10), "\n")

cat("Mean(y_hat) == mean(y): ",

isTRUE(all.equal(mean(fitted(fit)), mean(wage1$wage))), "\n")

```

---

## Goodness of Fit: A Geometric Derivation

Because $\hat{\mathbf{u}} \perp \hat{\mathbf{y}}$ — and because the column of ones in $\mathbf{X}$ forces $\hat{\mathbf{u}} \perp \mathbf{1}$, which means $\bar{\hat{u}} = 0$ and hence $\bar{\hat{y}} = \bar{y}$ — we can work with demeaned vectors.

Define $\tilde{\mathbf{y}} = \mathbf{y} - \bar{y}\mathbf{1}$ and $\tilde{\hat{\mathbf{y}}} = \hat{\mathbf{y}} - \bar{y}\mathbf{1}$. Since $\hat{\mathbf{u}} = \mathbf{y} - \hat{\mathbf{y}}$, we have:

$$

\tilde{\mathbf{y}} = \tilde{\hat{\mathbf{y}}} + \hat{\mathbf{u}}

$$

Squaring both sides (taking inner products) and using $\tilde{\hat{\mathbf{y}}}'\hat{\mathbf{u}} = 0$ (orthogonality — verify: $\hat{\mathbf{y}}'\hat{\mathbf{u}} = \boldsymbol{\beta}'\mathbf{X}'\hat{\mathbf{u}} = 0$):

$$

\|\tilde{\mathbf{y}}\|^2 = \|\tilde{\hat{\mathbf{y}}}\|^2 + \|\hat{\mathbf{u}}\|^2

$$

$$

\underbrace{\sum_{i=1}^n (y_i - \bar{y})^2}_{SST}

= \underbrace{\sum_{i=1}^n (\hat{y}_i - \bar{y})^2}_{SSE}

+ \underbrace{\sum_{i=1}^n \hat{u}_i^2}_{SSR}

$$

This is the **Pythagorean theorem applied to the OLS decomposition** — it holds as an algebraic identity, not as an approximation, and follows directly from orthogonality.

::: {.callout-note}

## Coefficient of Determination

$$R^2 = \frac{SSE}{SST} = 1 - \frac{SSR}{SST}$$

$R^2$ is the squared cosine of the angle between $\tilde{\mathbf{y}}$ and $\tilde{\hat{\mathbf{y}}}$ in $\mathbb{R}^n$. It lies in $[0, 1]$.

:::

::: {.callout-important}

## $R^2$ Does Not Measure Causal Validity

A high $R^2$ does not imply a causal interpretation. The election spending example in Wooldridge has $R^2 = 0.856$ but is still a correlation. The wage–education regression has $R^2 = 0.165$ but its coefficient may be closer to a causal effect (especially after controlling for confounders).

:::

### The Standard Error of the Regression

We need to estimate $\sigma^2 = \text{Var}(u)$. The natural candidate is $SSR/n$, but this is biased because we "used up" $k+1$ degrees of freedom estimating $\boldsymbol{\beta}$. The unbiased estimator is:

$$

\hat{\sigma}^2 = \frac{SSR}{n - (k+1)} = \frac{\sum \hat{u}_i^2}{n - k - 1}

$$

For simple regression ($k = 1$): $\hat{\sigma}^2 = SSR / (n - 2)$.

The **standard error of the regression** (SER) is $\hat{\sigma} = \sqrt{\hat{\sigma}^2}$, reported as `sigma` in `glance()`. It measures residual spread in the units of $y$.

---

## Running Example: Returns to Education

```{r}

#| label: wage1-glimpse

data("wage1", package = "wooldridge")

wage1 |>

select(wage, educ, exper, female, nonwhite) |>

datasummary_skim()

```

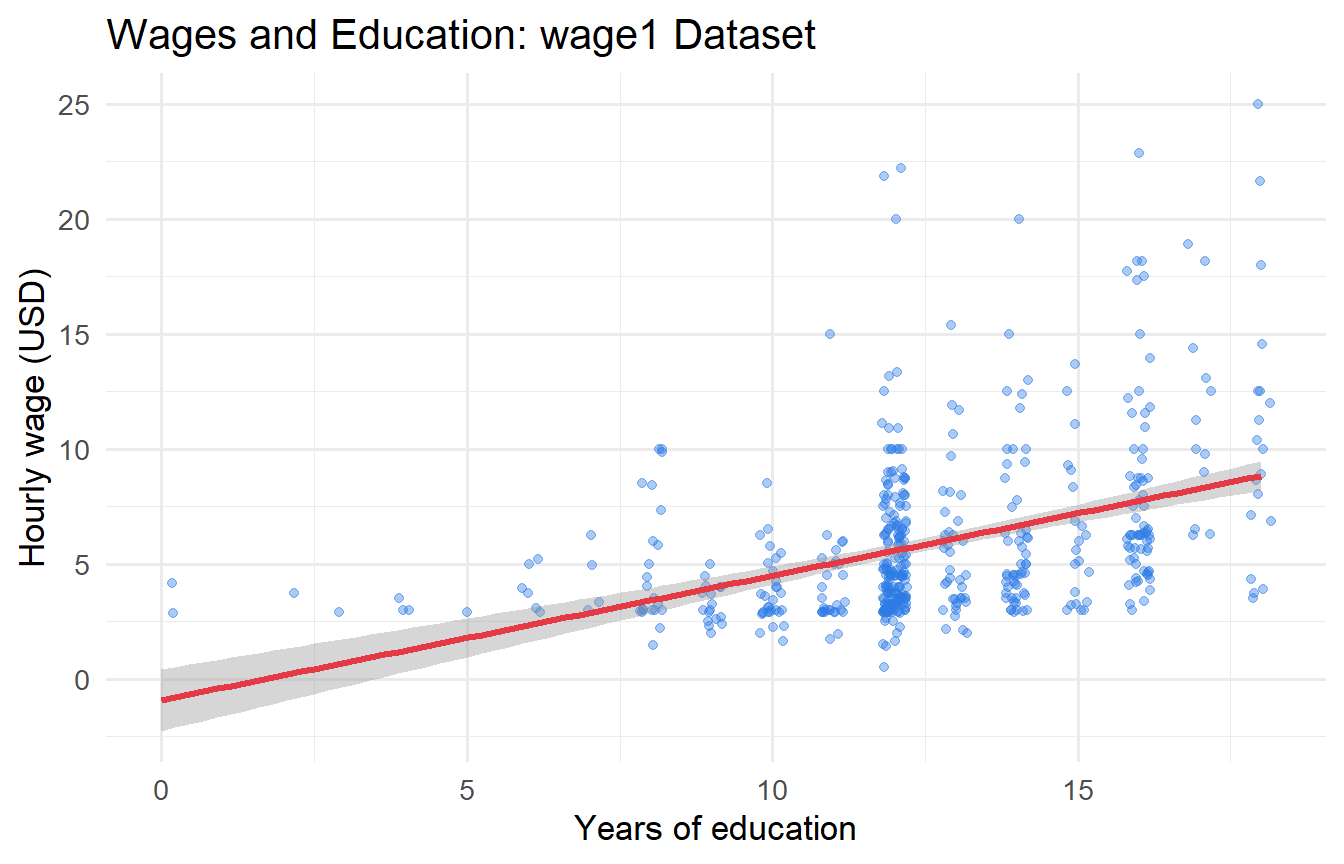

```{r}

#| label: fig-wage-educ

#| fig-cap: "Hourly wages and years of education. Line = OLS fit with 95% confidence band."

ggplot(wage1, aes(x = educ, y = wage)) +

geom_jitter(alpha = 0.4, width = 0.2, colour = "#2c7be5") +

geom_smooth(method = "lm", colour = "#e63946", linewidth = 1.2, se = TRUE) +

labs(x = "Years of education", y = "Hourly wage (USD)",

title = "Wages and Education: wage1 Dataset")

```

### Fitting and Reading OLS Output

```{r}

#| label: slr-wage

fit_slr <- lm(wage ~ educ, data = wage1)

tidy(fit_slr, conf.int = TRUE)

```

```{r}

#| label: slr-wage-glance

glance(fit_slr) |> select(r.squared, adj.r.squared, sigma, nobs)

```

- **Intercept** $(\hat{\beta}_0 \approx `r round(coef(fit_slr)[1], 2)`)$: Predicted wage with zero years of education. Interpret with caution — this is outside the support of the data.

- **Slope** $(\hat{\beta}_1 \approx `r round(coef(fit_slr)[2], 2)`)$: Each additional year of schooling is associated with \$`r round(coef(fit_slr)[2], 2)` more per hour on average.

- **$R^2 \approx `r round(glance(fit_slr)$r.squared, 3)`$**: Education explains `r round(glance(fit_slr)$r.squared * 100, 1)`% of the variation in wages. A low $R^2$ here is not a problem; many factors other than education affect wages.

- **SER $\approx `r round(glance(fit_slr)$sigma, 2)`$**: Residuals are on average \$`r round(glance(fit_slr)$sigma, 2)` away from the fitted line.

### Manual Computation and Verification

```{r}

#| label: ols-manual

wage1 |>

summarise(

x_bar = mean(educ),

y_bar = mean(wage),

cov_xy = sum((educ - mean(educ)) * (wage - mean(wage))),

var_x = sum((educ - mean(educ))^2),

beta_1 = cov_xy / var_x,

beta_0 = y_bar - beta_1 * x_bar

)

```

```{r}

#| label: ols-matrix

# Matrix form: beta_hat = (X'X)^{-1} X'y

y_vec <- wage1$wage

X_mat <- cbind(1, wage1$educ)

beta_matrix <- solve(t(X_mat) %*% X_mat) %*% (t(X_mat) %*% y_vec)

round(beta_matrix, 4) # identical to lm() output

```

All three routes — closed-form formula, `lm()`, and matrix algebra — agree exactly.

### Verifying the Decomposition

```{r}

#| label: r-squared-manual

aug <- augment(fit_slr)

SST <- sum((aug$wage - mean(aug$wage))^2)

SSE <- sum((aug$.fitted - mean(aug$wage))^2)

SSR <- sum( aug$.resid^2)

cat("SST:", round(SST, 2), "\n")

cat("SSE:", round(SSE, 2), "\n")

cat("SSR:", round(SSR, 2), "\n")

cat("SST == SSE + SSR:", isTRUE(all.equal(SST, SSE + SSR)), "\n")

cat("R-squared:", round(SSE / SST, 4), "\n")

```

### Residual Diagnostics

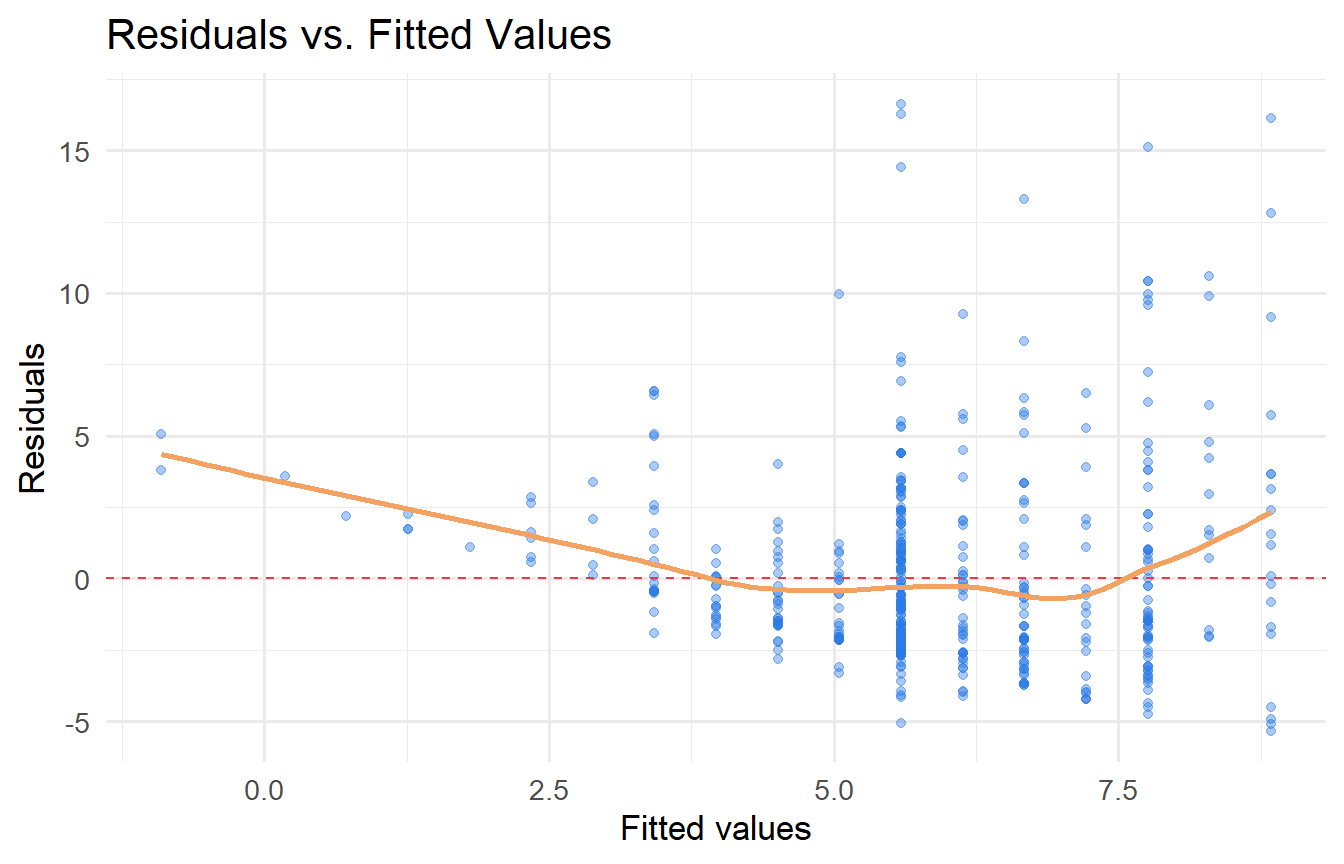

```{r}

#| label: fig-residuals

#| fig-cap: "Residuals versus fitted values. A pattern here signals model misspecification."

aug |>

ggplot(aes(.fitted, .resid)) +

geom_point(alpha = 0.4, colour = "#2c7be5") +

geom_hline(yintercept = 0, linetype = "dashed", colour = "#e63946") +

geom_smooth(se = FALSE, colour = "#f4a261", linewidth = 1) +

labs(x = "Fitted values", y = "Residuals",

title = "Residuals vs. Fitted Values")

```

The spread of residuals increases slightly with fitted values — a hint of heteroskedasticity that we return to in Chapter 9.

---

## Multiple Regression: A Preview

With two regressors the PRF becomes $E[y \mid x_1, x_2] = \beta_0 + \beta_1 x_1 + \beta_2 x_2$.

The **partial effect** of $x_1$ holding $x_2$ fixed is $\Delta \hat{y} = \hat{\beta}_1 \Delta x_1$. That is, $\hat{\beta}_1$ estimates the effect of $x_1$ on $y$ **after removing the variation in $y$ attributable to $x_2$**.

```{r}

#| label: mlr-preview

data("wage2", package = "wooldridge")

fit_iq <- lm(wage ~ educ + IQ, data = wage2)

modelsummary(

list("SLR (educ only)" = lm(wage ~ educ, data = wage2),

"MLR (educ + IQ)" = fit_iq),

stars = TRUE,

gof_map = c("nobs", "r.squared"),

title = "Education and IQ as Determinants of Wages"

)

```

Including IQ as a control reduces the education coefficient substantially. The SLR coefficient was picking up intelligence: smart people both acquire more education **and** earn more. Once IQ is held constant, the estimated return to education is smaller and represents a more credible partial effect.

---

## Tutorials

**Tutorial 3.1** Using `wooldridge::wage1`:

a. Regress `wage` on `exper` (experience). Report and interpret $\hat{\beta}_0$ and $\hat{\beta}_1$.

b. What is the predicted wage for someone with 10 years of experience?

c. What is $R^2$? Is it higher or lower than the education regression? What does this tell you?

::: {.callout-tip collapse="true"}

## Solution

```{r}

#| label: ex3-1

fit_exper <- lm(wage ~ exper, data = wage1)

tidy(fit_exper, conf.int = TRUE)

predict(fit_exper, newdata = tibble(exper = 10))

glance(fit_exper) |> select(r.squared)

```

- $\hat{\beta}_0 \approx `r round(coef(fit_exper)[1], 2)`$: predicted wage with zero experience.

- $\hat{\beta}_1 \approx `r round(coef(fit_exper)[2], 3)`$: each additional year of experience adds approximately \$`r round(coef(fit_exper)[2], 3)` to the hourly wage.

- Predicted wage at 10 years: \$`r round(predict(fit_exper, newdata = tibble(exper = 10)), 2)`.

- $R^2$ from experience: `r round(glance(fit_exper)$r.squared, 3)`, lower than the education regression (`r round(glance(fit_slr)$r.squared, 3)`). Education explains more cross-sectional variation in wages than experience does.

:::

---

**Tutorial 3.2** Verify the geometry of OLS numerically. Use any three-observation dataset of your choice (or the house example from Section 5).

a. Construct $\mathbf{y}$, $\mathbf{X}$, and compute $\hat{\boldsymbol{\beta}} = (\mathbf{X'X})^{-1}\mathbf{X'y}$ by hand in R.

b. Verify that $\mathbf{X'}\hat{\mathbf{u}} = \mathbf{0}$.

c. Compute $\mathbf{P}_X$ and $\mathbf{M}_X$. Check that they are idempotent and orthogonal to each other.

d. Verify Pythagoras: $\|\tilde{\mathbf{y}}\|^2 = \|\tilde{\hat{\mathbf{y}}}\|^2 + \|\hat{\mathbf{u}}\|^2$.

::: {.callout-tip collapse="true"}

## Solution

```{r}

#| label: ex3-2

y <- c(10, 4, 6)

X <- cbind(1, c(4, 1, 1))

# (a) OLS via matrix formula

beta_hat <- solve(t(X) %*% X) %*% (t(X) %*% y)

y_hat <- X %*% beta_hat

u_hat <- y - y_hat

cat("beta_hat:", round(beta_hat, 4), "\n")

# (b) Orthogonality

cat("X'u_hat:", round(t(X) %*% u_hat, 10), "\n")

# (c) Projection matrices

n <- length(y)

P <- X %*% solve(t(X) %*% X) %*% t(X)

M <- diag(n) - P

cat("Idempotent P: ", max(abs(P %*% P - P)) < 1e-10, "\n")

cat("Idempotent M: ", max(abs(M %*% M - M)) < 1e-10, "\n")

cat("P orthog. to M:", max(abs(P %*% M)) < 1e-10, "\n")

# (d) Pythagorean decomposition

ybar <- mean(y)

SST <- sum((y - ybar)^2)

SSE <- sum((y_hat - ybar)^2)

SSR <- sum(u_hat^2)

cat("SST:", round(SST, 4), " SSE:", round(SSE, 4), " SSR:", round(SSR, 4), "\n")

cat("SST == SSE + SSR:", isTRUE(all.equal(SST, SSE + SSR)), "\n")

```

:::

---

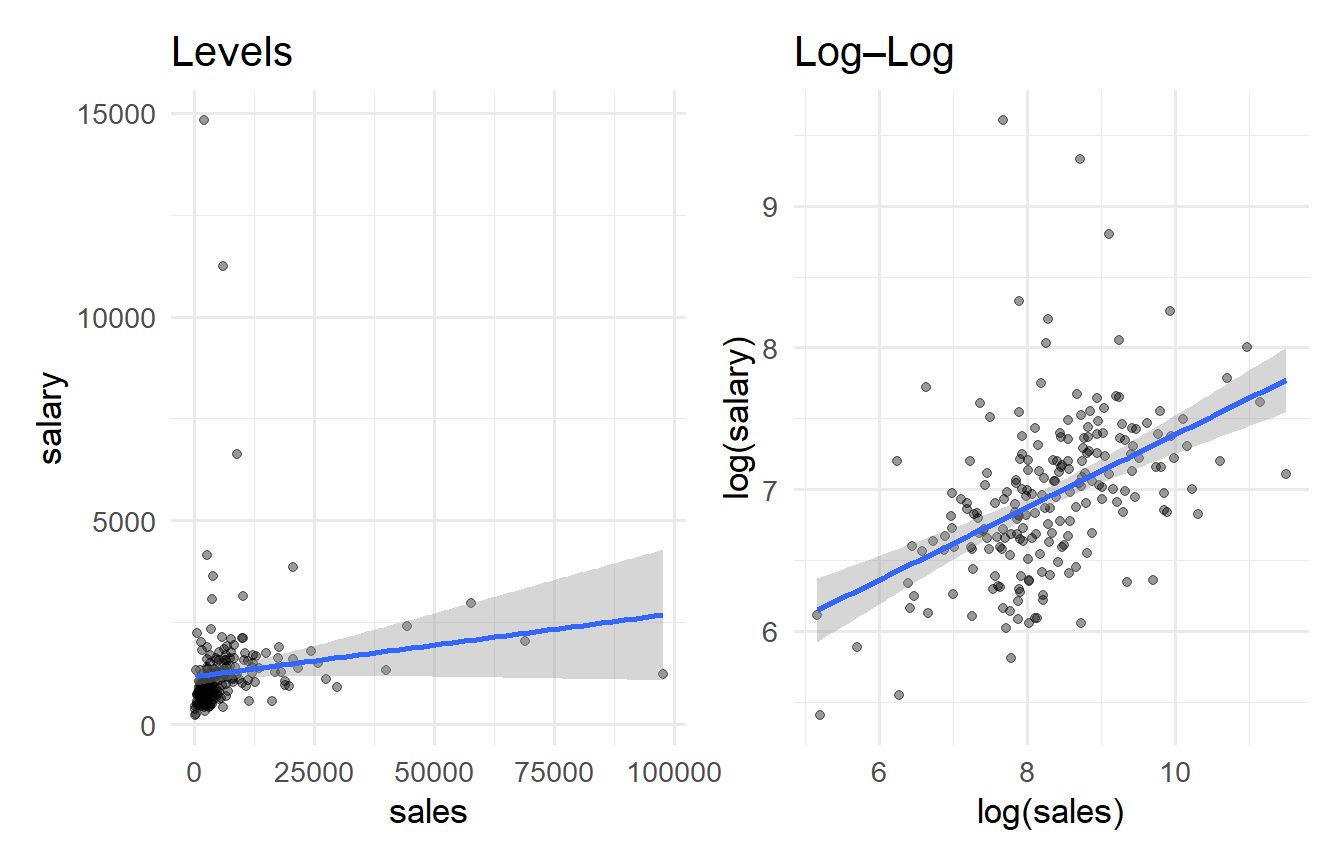

**Tutorial 3.3** Using `wooldridge::ceosal1`, regress CEO salary (`salary`) on firm sales (`sales`).

a. Interpret the slope coefficient.

b. Does the linear fit look appropriate? (Plot salary vs. sales.)

c. Regress `log(salary)` on `log(sales)`. How does the slope interpretation change?

::: {.callout-tip collapse="true"}

## Solution

```{r}

#| label: ex3-3

#| fig-cap: "CEO salary on sales: levels vs. log–log."

data("ceosal1", package = "wooldridge")

fit_levels <- lm(salary ~ sales, data = ceosal1)

fit_logs <- lm(log(salary) ~ log(sales), data = ceosal1)

p1 <- ggplot(ceosal1, aes(sales, salary)) +

geom_point(alpha = 0.4) + geom_smooth(method = "lm") +

labs(title = "Levels")

p2 <- ggplot(ceosal1, aes(log(sales), log(salary))) +

geom_point(alpha = 0.4) + geom_smooth(method = "lm") +

labs(title = "Log–Log")

p1 + p2

modelsummary(list("Levels" = fit_levels, "Log-Log" = fit_logs),

stars = TRUE, gof_map = c("nobs", "r.squared"))

```

In the log–log model, $\hat{\beta}_1$ is an **elasticity**: a 1% increase in sales is associated with approximately `r round(coef(fit_logs)[2], 3)`% increase in salary. The log–log specification fits considerably better because both variables are right-skewed; the levels regression is distorted by outliers.

:::